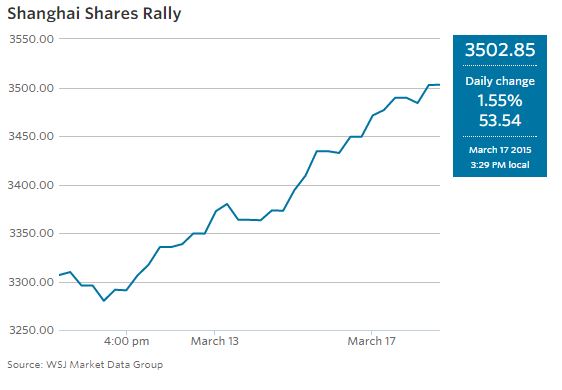

Chinese shares saw a rally the past few days after Premier Li Keqiang reassurance that the government will intervene to ensure healthy growth and employment. Chinese gains lead Asia-Pacific and come at a time of global economic uncertainty. Strong appreciation of the US dollar in the face of the Fed’s plans to raise interest rates gives mix signals. The global economy is also yet to see how quantitative easing in Europe will affect slowly consumption. These trends have weighed in part on China’s, resulting in the government cutting interest rates twice and driving down the yuan in order to ramp up exports.

The modest gains do not point to any significant macro-trend in China; however, Mr. Li’s committal to intervention indicates that the Chinese government will continue to stimulate. China’s FDI (foreign direct investment) fell nearly 30% this month. While FDI is season/cyclical by nature, there are concerns in Asia that higher Fed interest rates and European headwinds will draw money out of China. In turn, China must be able to stimulate its own economic transition into a normalized developed economy. China’s economy and stock market remain flagships in Asia, such that the economies of Taiwan, the Philippines, South Korea, etc. are heavily tied to China. It is important to see China in this global context with the US, Eurozone, and Asia.

Source: http://www.wsj.com/articles/china-shares-lead-gains-in-asia-on-stimulus-hopes-1426474637

The decline of foreign investment in China may be a result of increasing labor prices. Foreign companies who previously outsourced to China for manufacturing needs are now looking to SE Asian countries with lower labor costs.

For the past 20 years foreign investment has been very modest (2-3%?) relative to domestic sources of investment funds, even in formal industry.

As to stock prices, is the level rational? What are dividend payout rates? price-earnings ratios? Do these make sense given likely growth rates?

Even if central government officials use the term “stimulus” that is surely short-term in focus, but firms (and shareholders) are in it for the long haul, so that’s a (near-term) blip in the revenues that fix the net present value of a firm, or rather a firm’s shares. Unless you believe you can find greater fools in a timely manner, you should never buy shares in a firm at a price above that present value.