Sara Hsu, in a post for the blog “Naked Capitalism,” asserts that borrowing is being used to prop up Chinese GDP statistics. Total debt of Chinese corporations, local, provincial, and state governments has reached 85 trillion yuan. Hsu, an Economics Professor in the SUNY system, argues local governments have wanted to appear to be stimulating growth despite a slowing real production. Government and corporate debt, issued primarily through securitized loans known as “entrusted” or “trust” loans, have been used to mask economic shortcomings.

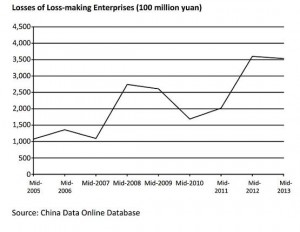

Economic news from China is increasingly less rosy. The jump in the number of loss-making enterprises from 2,00 to 3,500 in the past 2 years and a significant drop in year on year growth in industrial value added were used as examples of this trend. Hsu argues a credit crisis is possible. How likely is such an event?

I identified similar risks in my blog post “Credit Bubble Imminent?” on 9/11/13. China’s debt levels are high, even in excess of other fast growing countries when they experienced a credit crisis. If China is reporting fraudulent or manipulated GDP figures as has been sometimes argued, and does not act to slow credit growth, a sovereign debt crisis seems possible. Such a crisis is unlikely, but should not be ruled out by investors.

Such an event would devastate citizens as unemployment skyrockets and personal savings are wiped out, causing poverty and unrest to rise. Hsu argues that controlled deleveraging and protecting/shrinking vulnerable financial institutions could preclude such an event. Will the Chinese government will be able to successfully manage this changing economic situation?

Source: http://www.nakedcapitalism.com/2013/09/chinas-ultimate-debt-holders-not-the-borrowers.html

If fiscal policy is indeed used to stimulate an economy, then the counterpart is debt. (If you tax to cover expenditures, you don’t get stimulus.) Of course you also need to look at changes in fiscal policy, not steady levels.

But whether it’s a credit bubble depends on whether there are adequate savings (remember the paradox of thrift from Econ 102?). And if the fiscal stimulus is used to create something that increases productive capacity, public investment (a road, housing, railroads but not “white elephant” opera houses and unnecessarily luxurious and kickback-laden public buildings), well then there will be more resources down the road that can be taxed.

That doesn’t preclude things that look like “bubbles” in specific markets. After all, how do you price a long-lived asset when an economy is growing at 8% pa? What will housing be worth in 20 years? So miscalculations are inevitable. And yes, there are such things as bubbles. But we need to be slow to use our experience of appropriate prices to judge what might make sense in China.

I don’t think China per se would be the cause of a popped bubble for its own growth and asset prices (property/debt/other assets). However, if global bond investors get spooked over a sovereign that defaults and markets undergo serious stress then China could be more at risk of being closed out of the debt markets. While the research of Reinhart and Rogaoff has been under scrutiny and somewhat discredited, I do think the pattern of financial crises alternating with sovereign debt default crises was interesting. While China has a high savings rate, would that be able to avert problems if liquidity plummeted along with investor faith in sovereign debt markets too? I won’t claim to have the answer.